Tom Green

Innovation on the farm

Eli Whitney’s cotton gin, McCormick’s reaper, Ford’s farm tractor, agriculture has been acquiring labor-saving devices since human’s first went from being hunter-gatherers to land-tilling food growers and livestock raisers.

The work is hard, the hours long, the weather’s fickle, the harvest is a do-or-die must, so why wouldn’t any right-thinking human brain want to conjure up a few new ways to lessen the load?

And that’s just what has happened for millennia. Today, robots and other autonomous machines prowling fields and orchards are just the newest incarnations in farming’s eternal quest for ease of doing business with Mother Earth.

And the “land-tilling and livestock raising” that humans created for themselves, they have been trying to wiggle their way out of for hundreds of years. Who wants the grief of farming when gleaming cityscapes beckon and the allure of industry and business are so damn attractive? Even the meatpacking, city misery of Upton Sinclair’s The Jungle offered a slim chance of escape to a better life.

Not so farm life, it’s forever, unless you get conscripted into someone’s army or a machine comes along and makes your work redundant, which is exactly what has happened.

Farm workers don’t need their arms twisted to encourage fleeing the farm; they’ve been leaving by the millions never to return, except for holidays. Barely 1.5 percent of America’s population are farmers; in Germany it’s about 4 percent. China has over 400 million farm workers; ten years ago, China had 700 million. That’s an incredible 30 million a year making a dash for the cities.

But still, we all have to eat. Someone has to feed us. And the global appetite is on the grow…exponentially:

“The human population is expected to climb to 9.8 billion by 2050 and 11.2 billion by 2100, according to the United Nations. To feed the world — with less land, fewer resources and in the face of climate change — farmers will need to augment their technological intelligence.” —NYT: A Growing Presence on the Farm: Robots

See related: Feeding Asia: Robots, Automation & Four+ Billion Mouths to Feed

From farm to chopsticks: Not enough land, not enough water, too few farmers, and $470 billion in annual food spoilage

Steel-collar farmhands

Erik Pekkeriet of Wageningen University & Research predicts that “10 to 20 years from now, robots will do all the repetitive work in the agricultural sector.”

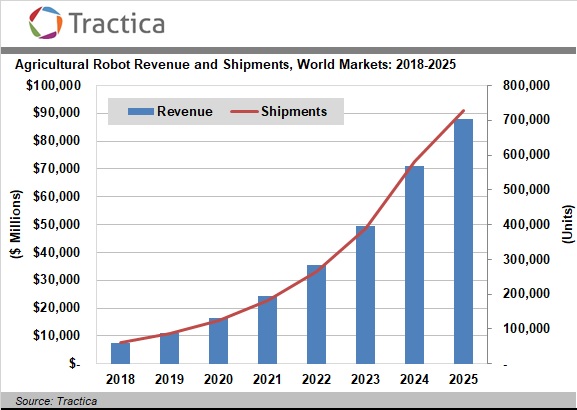

Maybe sooner. Research forecasters are reporting “agricultural robots to develop rapidly (2020-2025)” topping out in 2025 at $20 billion. Amazing, especially so since the market was only $3.4 billion in 2018.

Maybe that’s what is generating all the recent media buzz on robot farming. To nearly triple growth is definitely eye-popping. Something is definitely going on

Tractica has even produced a chart showing the coming inflection point: 2021 looks like the jump-off point for agricultural robot shipments to drastically increase (see chart).

So, what’s happening?

David Frabotta, writing in PrecisionAG, has what looks like the most sound take on robots in agriculture with his article: Agricultural Robotics Segment Maturing Amid Intermittent Commercialization. Perfect title!

Isn’t this what we’re seeing: “In agriculture, technology introductions have sputtered for numerous reasons: A prolonged global recession dating back to 2008 slowed investment, lack of interoperability standards created disparate ecosystems, and products focused too much on the technology instead of addressing real-world grower problems and workflows.

“But those dynamics are changing for the better, and real change is starting to creep into the market as leading companies are on the cusp of changing the trajectory of innovation and adoption.

“Here’s why: Partnerships and collaboration among leading companies are accelerating innovation and speed to market. Start-up culture historically has been a lonely endeavor as inventor companies cautiously guard proprietary advancements amid competition from inside and outside of agriculture.

“But that is changing for a couple reasons, primarily because technical and operational challenges are too complex for any one company to create a complete platform. Robotics, which implies autonomy, requires sophisticated mechanization and software. Mechanization requires a supply chain, and software requires interfaces for interoperability. Many companies have tried to create a ground-up platform internally, but the complexity has rendered this approach unfeasible.

“It shows a great deal of business maturation for start-ups to seek partnerships and joint ventures to accelerate product life cycles and commercialization, and that business maturity will help garner more investment.”

See related: Maybe we should call it Neo-Ag

Neo-Ag: Farming with Robots, AI & Ingenuity

A “Google moment” for agriculture that’s ultra-precise, data-driven, and brimming with special-purpose robots is also powering lots of new thinking