End of the road

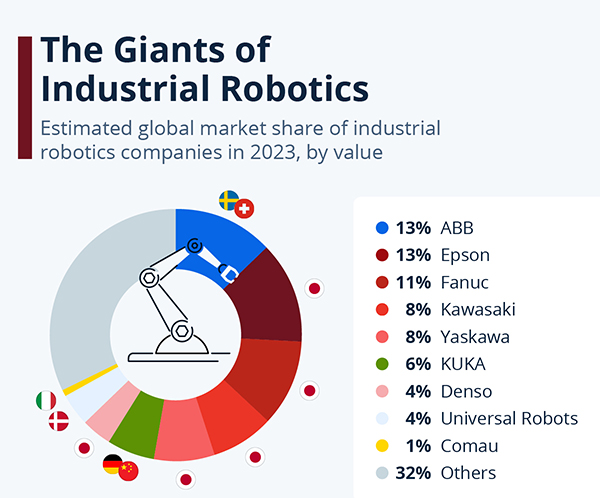

Arguably, the robot builder that kicked off the modern age of robotics and revolutionized manufacturing in 1974 (under its former name ASEA), ABB’s Björn Weichbrodt and his team invented the IRB6, the world’s first all-electric, microprocessor-controlled industrial robot. Thereafter, ABB’s growing line of industrial robots, vaulted the Zurich-based conglomerate to leadership in world market share, according to Statista (December 2024), along with Epson and FANUC (see chart). Then, along came a day in October of 2025 when things unraveled a bit. What happened?

After some five decades of building robots, ABB Group bailed on it all on October 8, 2025, when it agreed to sell its entire robotics division to Japan’s SoftBank Group for $5.3 billion. marking the end of an era for the robot division as one of robotics pioneering and legendary companies.

The decision to sell a business that was once a core part of your identity is a de facto admission that you cannot, or do not wish to, shoulder the immense investment and cultural shift required to compete in the next phase. It’s a paradigm shift for robotics that tends to acknowledge that the future of robotics lies in AI and ecosystem platforms, areas where ABB was lagging and a company like SoftBank (with its Vision Fund and tech investments) theoretically has an advantage. SoftBank has little experience or expertise in developing, scaling or deploying robots, but it has some powerful assets that might fair very well with ABB’s product line. An AI future could well be quite exciting for SoftBank.

As one analyst noted, “This move may push ABB’s competitors, particularly the other ‘Big 4’ players, to accelerate collaborations with AI and software companies or bring in investors, ensuring they have the resources to stay competitive in the AI-driven robotics space”.

“The elephant is slow to mate,” wrote D.H. Lawrence. And in the case of ABB, it was glacial when it came to adopting new innovations in robotics, especially, its most recent challenge with artificial intelligence (AI), GenAI, and Physical AI converging with robotics.

Asian Robotics Review has followed and reported on ABB for over ten years in a series of articles that portray a great robotics company waffling on product line upgrades as we observed ABB’s slow-to-mate performance. Case in point: The company’s YuMi, GoFa, SWIFTI cobots were a slowly evolving mystery rolled through the last decade or two. YuMi was cross-bred between ABB’s original cobot FRIDA (for Friendly Robot for Industrial Dual-Arm) and the sleek industrial arm, Roberta, famously designed by the German mechanical wizard, Bernd Gombert, and immediately acquired by ABB after its first showing at AUTOMATICA in 2014. However, that was a good five years after Universal Robots introduced the world to cobots in 2008. The Cobotics World catalog now lists 182 cobot models from 58 cobot manufacturers. What took ABB until 2021 to birth new cobots? Similarly, it was ABB’s tardy response to the rush for AMRs, long after the global logistics map was jammed with AMR maker logos that industrial robot giant ABB arrived so late to scoop up Spanish AMR maker ASTI Mobile Robots.

ABB’s belated recognition of autonomous mobile robots (AMRs) as a critical technology segment is another case in point. The global AMR market exploded from $1.97 billion to a projected $8.70 billion by 2028, growing at 23.7% CAGR, yet ABB had no organic capabilities in this rapidly expanding sector.

To catch up, ABB acquired Spanish AMR manufacturer ASTI in 2021, followed by Swiss startup Sevensense in January 2024 for their AI-based Visual SLAM navigation technology. These acquisitions represented a big pill to swallow—ABB was forced to buy capabilities that competitors had developed internally years earlier. The company’s first meaningful AMR product, the Flexley Tug T702, didn’t arrive until 2024, while competitors like Mobile Industrial Robots (now part of Teradyne) and others had already entered the market years before.

The acquisition strategy revealed ABB’s fundamental problem: it had become a reactive follower rather than a proactive innovator. As Alfonso González, ABB’s global managing director for AMR, admitted, the company was trying to differentiate through “high precision hardware, easy to use software and AI based learning models”—essentially playing catch-up with features that leading AMR companies had already commercialized.

Curious trail to the parachute

The roots of ABB’s robotics divestment trace back to the devastating 2009 financial crisis, when the division hemorrhaged $300 million in operating losses. While then-CEO Ulrich Spiesshofer successfully turned the unit around in subsequent years, the fundamental structural challenges that emerged during that crisis were never fully resolved. The robotics division consistently underperformed compared to ABB’s other businesses, achieving only a 12.1% EBITDA margin in 2024—significantly below ABB’s group average of 18.1% and far trailing competitors like FANUC, which maintains gross profit margins between 30-35%.

Omdia research analysis provided crucial insight into ABB’s predicament: “ABB is spinning off its robotics unit to refocus on core strengths. Facing stiff competition from agile rivals and tech disruptors, the new entity must scale.” This assessment proves remarkably prescient. ABB’s robotics business model had become fundamentally misaligned with market realities—too expensive to compete with Chinese manufacturers, too slow to match FANUC’s volume-driven approach, and too dependent on complex, custom-integrated systems that ate into margins and hindered scalability.

Doing business in China since 1975 and realizing 30% of its corporate profits there, it must have come as a particularly disconcerting moment to learn of Made in China 2035’s big push to build out its own indigenous robotics industry. The handwriting was on the wall: the Chinese had had enough of relying on foreign robot makers and their high prices. By 2024, China was making over 50% of its own robots (and buying over 34% of them). See also: The Rise of China’s Robotics Industry.

The Competitive landscape that left ABB behind

ABB’s struggles reflect broader seismic shifts in the global robotics industry. While ABB maintained its position as the world’s second-largest industrial robot maker, this ranking masked profound competitive weaknesses. Chinese manufacturers like Inovance, Estun, and Efort have revolutionized the market by delivering highly adaptable robots at speeds and prices that ABB simply cannot match. These companies have captured over a third of China’s domestic robotics market by undercutting foreign competitors by 20-30% while also providing hyper-responsive local service.

Meanwhile, established Japanese competitors like FANUC have thrived through volume-based, standardized robot sales with minimal customization, enabling unmatched margin consistency. This performance gap illustrates the fundamental difference in business models: while FANUC focuses on high-volume, standardized solutions, ABB remained wedded to complex, engineering-heavy custom integrations that proved impossible to scale profitably.

Technology lag in the AI revolution

Perhaps most damaging to ABB’s competitive position was its sluggish adaptation to artificial intelligence and emerging robotics technologies. The company was notably slow to introduce collaborative robots after its early YuMi success, only launching the GoFa and SWIFTI cobot lines in 2021—years after competitors had established market positions. Even then, these products failed to generate the market traction needed to revitalize the division.

ABB’s belated recognition of the AI revolution is evident in its recent attempts to catch up. Just weeks before announcing the SoftBank sale, ABB invested in LandingAI and launched OmniCore EyeMotion, AI-enabled machine vision software. However, these moves came too late—the company was already years behind competitors who had integrated AI capabilities into their core offerings.

Financial reality and strategic realignment

The financial mathematics behind ABB’s divestment are stark and unforgiving. Despite generating $2.3 billion in revenue in 2024, the robotics division represented only 7% of ABB’s total revenues while consuming disproportionate management attention and capital resources. More problematically, revenues had declined from $2.5 billion in 2023, indicating the division was contracting even as the global robotics market expanded.

ABB Chairman Peter Voser candidly acknowledged the strategic logic: “SoftBank’s offer has been carefully evaluated by the board and executive committee and compared with our original intention for a spin-off. It reflects the long-term strengths of the division, and the divestment will create immediate value to ABB shareholders”. This diplomatic language cannot obscure the underlying reality—ABB must have concluded that its robotics division was worth more to SoftBank than to ABB itself.

The $5.3 billion sale price, while substantial, represents an EV/EBITDA multiple of approximately 17.2x—a modest premium that reflects both the division’s technological assets and its operational challenges. For ABB shareholders, the transaction promises immediate value realization while eliminating the ongoing drag of an underperforming division.

SoftBank’s AI ambitions and physical AI strategy

SoftBank’s acquisition of ABB Robotics aligns perfectly with Chairman Masayoshi Son’s views on “Physical AI” as its next frontier, seeking to combine artificial intelligence with robotics to create revolutionary automation solutions. ABB’s robotics division, despite its operational challenges, brings globally recognized technology, extensive customer relationships, and manufacturing capabilities that complement SoftBank’s existing robotics investments in companies like Berkshire Grey, AutoStore, and Agile Robots.

Son’s vision extends beyond traditional industrial robotics to encompass a future where AI-powered robots transform manufacturing, logistics, and service industries. ABB’s established presence in automotive, electronics, and general manufacturing provides SoftBank with immediate market access and customer credibility that would take years to build organically.

Conclusion: A strategic necessity, not choice

ABB’s sale of its robotics division to SoftBank represents the culmination of competitive pressures that had been building for over a decade. Despite the division’s historical significance and substantial revenues, ABB’s leadership correctly recognized that the company lacked either the strategic focus or financial resources needed to compete effectively against specialized robotics companies and well-funded technology giants.

The 16-year journey from near-bankruptcy in 2009 to strategic divestment in 2025 illustrates the challenges facing traditional industrial companies in an era of rapid technological evolution. SoftBank’s acquisition provides ABB Robotics with the focused leadership, AI expertise, and financial resources needed to compete in the next phase of industrial automation.