The year 2020, with its economy-crushing COVID pandemic, liberally sprinkled with lots and lots of uncertainty, has cast a mega-spotlight on the use of automation in warehouses worldwide. Whether logistics is adapting to new social distancing rules, or under pressure to distribute a higher volume of essential goods, or struggling to meet same day delivery or even trying to add more remote work capabilities, the rapid churn of SKUs through warehouses is without precedent.

It’s completely changing what it means to move and store goods from one place to another.

For a few years now the armies of warehouse transformation have been massing and now seem more than ready to completely automate the global face of logistics.

The good folks at LogisticsIQ have put together a stellar look at what’s happening in their latest post-pandemic market research study, Warehouse Automation Market. The bottom line: It will reach a milestone of $30B by 2026, at a CAGR of ~14% between 2020 and 2026.

Key highlights

- Warehouse automation equipment suppliers and industry consultants expect broadly double-digit growth in sales driven by demographic changes, increased penetration in e-commerce and the advent of the Industrial IoT, that will drive demand for data analytics and automated operations, especially after COVID.

- Competitive landscape – There are 10 large and 10-20 medium-size companies operating in the material handling equipment space capable of delivering comprehensive automated warehouse solutions. Top 10 large companies (including Dematic, Daifuku, SSI-Schaefer, Honeywell Intelligrated, Knapp, Toyota, Muratec, Swisslog) are capturing more than 50% of market share although lots of start-ups are emerging in new categories like AMRs, Picking Robots, Micro-Fulfillment, Autonomy Service Providers etc.

- Service model importance increasing – Over the time as the installed base of automated warehouse solutions grows, industry players expect an increase in revenues from services and maintenance, which would have a positive impact on profitability as the service business typically has 15-20% operating margins, versus 3-5% margins for new equipment. It is expected to be ~$7B worth market by 2026.

- Business models are also changing considering the real time pain points of end-users for high capex. Businesses are increasingly intrigued with RaaS because of its flexibility, scalability, and lower cost of entry than traditional robotics programs. The business model for picker-as-a-service is usually on a per-pick basis, ranging from 6 cents to 10 cents per pick, while AMR-as-a-service is usually leased on a monthly basis, from US$711 per robot per month to several thousands of dollars per month, depending on the commitment period.

- Industry Consolidation – The past 3-4 years have seen an increase in consolidation amongst material handling equipment providers as traditional players see acquisition of technology leaders as an increasingly attractive way of positioning themselves in response to changing market trends. Acquisitions like KION (Dematic), KUKA (Swisslog), Toyota (Vanderlande, Bastian Solutions), Hitachi (JR Automation), Honeywell (Intelligrated, Transnorm), Korber (Cohesio Group), Teradyne (MiR, Energid, AutoGuide Mobile Robots) are just some of the examples of this consolidation.

Facts to know

- Global e-Commerce sales have grown at a CAGR of 20% over the last decade, reaching ~$3.5 trillion worldwide in 2019 and expected to grow to ~$7.5 trillion by 2026. The share of online retail sales has gone from ~2% of total to ~13%, and is further expected to reach ~22% by 2026

- Existing fully automated systems can reduce warehouse related labour costs by up to 65% and logistics-related spatial use by up to 60% at the same time as it increases the maximum output capacity.

- The adoption of technology is by no means uniform. While one-hour delivery is available when buying online in some parts of the U.S. and Europe, the average promised delivery time in Brazil is nine days. JD.com had a record-breaking Singles Day in 2019, with transaction volume exceeding CNY204 bn (US$29 bn), up by 27.9% on the previous year. Logistics played an important role, with 90% of areas achieving same-or next day delivery and 108% YOY increase in number of orders fulfilled by automated warehouses.

- Amazon Robotics automates the company’s fulfillment centers using more than 200,000 autonomous mobile robots, up more than 600% from 30,000 at the end of 2015. Last year, DHL announced an investment of $300 million to modernize 60% of it warehouses in North America with IoT and autonomous robots. Company also committed a deployment of 1,000 LocusBots for delivery fulfillment. The funds are earmarked to bring emerging technology to 350 of DHL Supply Chain’s 430 operating sites.

- Warehouse labour shortages are also an issue with peak labour demands occurring around major shopping holidays viz. Black Friday, Cyber Monday, Amazon Prime day, Thanksgiving Day and Singles Day. Warehouses have to hire temporary labour around these peak times to meet the customer delivery schedules. Supply chain robotics company Cainiao has installed 700 robots at China’s largest robot-run warehouse to process orders on Singles Day.

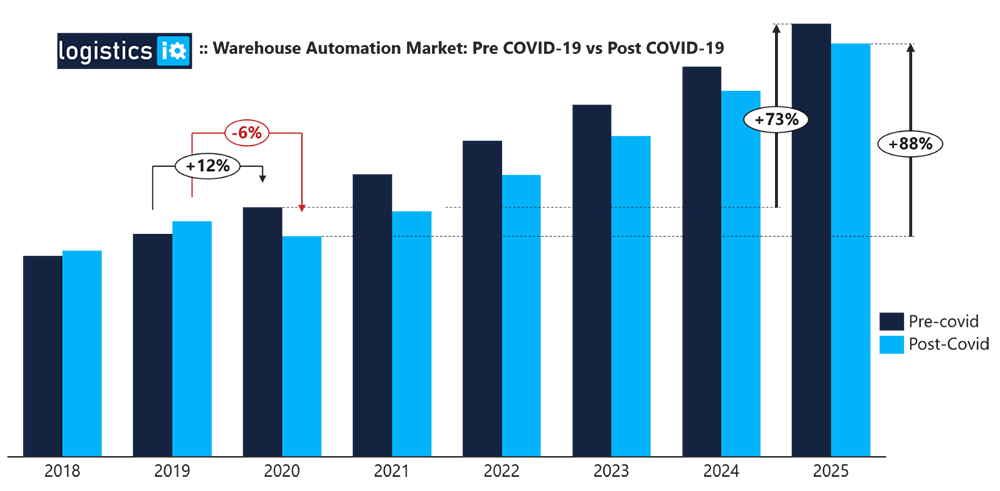

Compare and contrast: Here’s pre-COVID outlook from 2018-2019

LogisticsIQ’s post-pandemic version of Warehouse Automation Market report is having a detailed market analysis of more than 650+ players (part of our exclusive Market Map), 10 solutions, 7 industries and 30 countries along with 440 pages, 355 Market Tables, 210 Exhibits and 110 Company Profiles. Analysis is validated through 100+ in-depth interviews across the value chain with components and technology providers, system integrators & manufacturers and end-user industry verticals.

Take a look at the 650 companies vying for a share of warehouse automation:![]()