First, a quick look back (sorry)

If you are looking to invest in robotics again, put away your binoculars, the coast is clear. This is a most interesting time to invest; it may not come around again, ever! Don’t let it pass without serious consideration.

First off, remember this? It doesn’t take many memory cells to recall this totally gruesome event:

“The fastest fall in global stock markets in history and the most devastating crash since the Wall Street crash of 1929…And millions of investors lost 40 percent of their retirement in a matter of weeks.”

Yikes! That was horrible, especially if you owned a business; worse, a factory.

What about now? Things are taking shape that point to a new surge on the way for industrial robot and cobot sales. It could well be a blockbuster for those who buy into the movement early. The signs are there.

Lay of the land

In the near past by this time of year, we would already have seen scads of news reports effusively reporting on the large number of industrial robot sales in North America. To date, silence. And it’s loud!

Industrial robot and cobot sales escaped a down year in 2019 only to run headlong into the COVID pandemic where sales flatlined. At earnings calls, company execs tried to be future looking and confident, but sounded dour as they spoke. Some washed their remarks in dense corporate speak that seemed to make things worse. Very few were frank. Even the analysists in the audiences seemed to go easy on them. Everyone knew that the world was in a tough place; let’s not make it tougher.

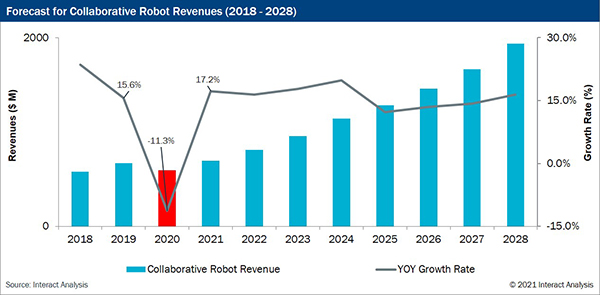

Interact Analysis: “Industrial robot shipments experienced negative growth for four consecutive quarters from mid-2018 onward. The decline in robot sales had narrowed by the beginning of 2020. Investment in industrial robots was projected to pick-up, with stronger growth expected through the year. Then, the outbreak of COVID-19 put the brakes on the return to growth.”

“The collaborative robot [cobot] market weathered a difficult 2019 due to a slow-down in the global economy which affected the important Asian market the most, and a tumultuous 2020, when the market saw negative growth for the first time – -11.3 percent in revenue terms, and -5.7% in shipment terms.”

It was sad listening to the earnings calls. Lots of humans were not building robots and cobots because lots of humans were not buying robots and cobots.

The Eurozone was just as bad off, mostly worse. In 2020, for example, the whole of the UK bought slightly over 1900 industrial robots for the entire year. By contrast, China bought 13,000 industrial robots monthly.

End users

When COVID hit the West, big manufacturers immediately pushed the pause button, idled their lines and laid off workers. Many reckoned, minus their employees, they had the wherewithal to weather storms for a short time; with government help, maybe longer. But who’s going to make the toilet paper, chicken cutlets, and the tanker trucks full of Clorox in order to fill empty aisles in supermarkets? The fortunes to be made were too great to pass up, many cranked up with socially distanced production lines.

Of course, “Never again such a disruption” was the cry from every boardroom, so they all tasked reassessment teams to hasten automation, both cyberphysical machines, RPA (robotic process automation), and wherever AI/ML would conveniently fit. In the U.S. The “Great Reset” is coming and “disruption-taming” robots are on the need-to-have list for everyone.

However, the “Great Reset” is a tough nut to crack. McKinsey reports that 84 percent of global executives believe innovation is extremely important, but only 45 percent have made significant headway, and only 6 percent of those execs are satisfied with their organization’s innovation performance.

The net-net is that pent-up demand for industrial robots is accelerating, the addressable audience is expanding, yet no one is buying them. They’re way not ready to pull the trigger to buy until Q4 2021. The exceptions being logistics, like Amazon, FedEx, DHL and anyone else in the delivery biz, because nothing short of a nuclear war is going to stop e-commerce, no matter how many thousands of human workers are needed to keep the brown boxes flowing.

Boardrooms want to buy robots, but none want to buy into a catastrophe. Logistics is a case in point. Who in their right mind these days will dump $10 million to $20 million into building out infrastructure for logistics robots? No one!

Especially when you can opt for an alternative like Locus Robotics’ machines that operate just fine in unstructured environments. Probably one of the many reasons Locus just picked up a cool $150 million in investment to expand. Locus went from start-up to unicorn status because it has winning tech, and now has eyes on going public. Other makers, and there are many similar to Locus, are selling machines.

Meanwhile, approximately 10.7 million Americans are out of work, nearly twice as many as before the pandemic struck, while The Organization for Economic Co-operation and Development (OECD) is reporting 45.5 million persons unemployed as of January.

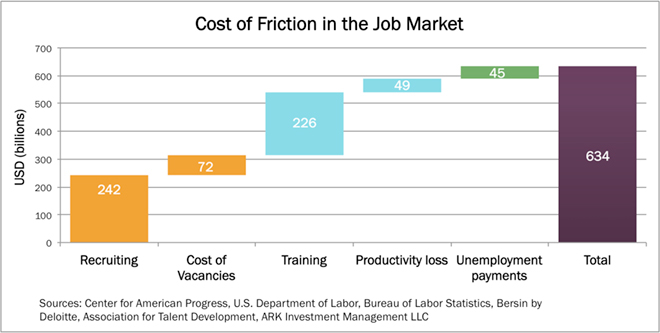

Experts say that upwards of 40 percent will not return to their original jobs, which has a hidden bonus for corporations. Automate, and corporations will never have to fear social distancing or the rigors of recruiting staff; and in the process, save a ton of money on hiring and training workers. ARK Invest reports that “Friction in the labor market costs the U.S economy more than $630B per annum.” Again, that’s annually! See chart below for the specifics.

There’s plenty of money there to switch off into robots and RPA. Looks like the best route is to jettison staff permanently. Throw them on the unemployment rolls, and instantly lose the Plexiglas and those expensively annoying safety rules.

That’s harsh medicine for employees to swallow, but it’s already happening and much more is to follow. It happened during the Great Recession (2008-2017) to six million workers. It’s happening again. The need for reskilling and upskilling workers will grow evermore critical.

Then comes Q4

Eventually, around Q4, the quest for more productivity and the waning of COVID, corporations will be enticed back into buying robots once again. The elevator will go up, and there will never be a time quite the same to invest in automation.

There’s wisdom in investing now in robotics, either buying equities (pure play or mixed) or in ETFs (Exchange Traded Funds). Automation is inevitable, and robots are the key drivers. It’s just a matter of time, and that time is drawing close.

The plight of SMEs

Pity the SME, the primary target for cobot sales. Hard-working individuals who love their businesses and their employees but are caught up in the vice grip of COVID and the economy. They are hanging on by their fingernails and near frantic about keeping the business that they worked so hard to start. For some it has been a lifetime of work.

Most have spent a backbreaking ton of money on Plexiglas walls and social distancing for their employees. There’s nothing left over for automation after those kinds of ongoing outlays. And government help is nice, but never enough. Each has to dig his or her own way back into the light.

The International Monetary Fund (IMF) looked at the health of SMEs in 17 nations: IMF Working Papers: COVID-19 and SME Failures. In the Eurozone, SMEs are its lifeblood. “In the European Union SMEs, consisting of firms with less than 250 employees, account for a striking 99.8 percent of all employer firms, 65 percent of private sector employment and 54 percent of private sector gross output.” If these folks go under, the Eurozone is going to be hurting big time.

Whether in the EU or North America, “SMEs are exposed to a major vulnerability – they are critically dependent on debt, especially bank loans, for financing. Under normal circumstances, typical liquidity shortages can be managed via short-term loans or working capital without endangering the survival of the business.” But not this time around. For anyone so vulnerable, taking on financing for automation via cobots, even if it would be beneficial for productivity and overhead, is unthinkable. For the immediate future, staying afloat is job #1.

It’s anguishing for SMEs to be in such a position. Each knows full well that competitors are out there readying to eat their lunch. Each knows that ultimately, they will be graded on their quality, productivity and price, and that they must not let their narrow advantage slip away. And each knows that some sort of automation is the answer. Most SMEs, 90 percent, according to the former CEO of Universal Robots—the world’s best-selling cobot, are unaware what a cobot actually is, let alone how to buy one.

That needs to change, especially if the forecast from Interact Analysis has a chance to materialize: “The company predicts that there will be a V-shaped rebound for the industry which will result in growth of nearly 20 percent in 2021, surpassing the 2019 market size. Thereafter up to 2028 there will be an annual growth rate of the order of 15-20 percent. Not as high as previously predicted, but healthy nonetheless.”

Talk about “growth of nearly 20 percent in 2021” is possible, but only because cobot sales flatlined in 2020. Any life looks good after a near-death experience.

Selling cobots to SMEs

SMEs can’t buy what they don’t know about. One big reason that cobots are not well known by SMEs is that, for the most part, they are sold like traditional industrial robots at trade shows. Problem there is that SMEs don’t attend trade shows in appreciable numbers. They are too busy with their own businesses to carve off funds and precious time to attend.

It may well be better to sell cobots door-to-door like vacuum cleaners. Knock on the front door, and when it opens, throw dirt on the floor and use the marvelous vac to clean it all up. That’s impressive. Whatever the cobot equivalent of door-to-door selling is needs a try. That’s how to get to the masses of onesie-twosie sales from SMEs that have a chance of leading to reorders for more.

Hyundai Robotics has an opportunity to make a different kind of sell. What if Hyundai Robotics teamed up with Hyundai Motors? Use a small corner of every Hyundai auto showroom to sell the Hyundai YL012 cobot. Hyundai Motors sells in 193 countries through 5,000 dealerships and showrooms. That’s a lot of cobot coverage. An SME might more easily nip off downtown for a look-see at a cobot than travel miles to a tradeshow, only to get lost in a maze of booths. Such an arrangement might even help with sales of automobiles. It sure as hell is a nice PR event for local media.

The International Federation of Robotics (IFR) reports that cobot sales represent a miniscule 3 to 4 percent of overall industrial robot sales. That’s pre-COVID! Cobots are wonderful machines with a vast addressable audience, but, unless something earthshaking blasts them into prominence, it’s hard to see sales rising above the “miniscule” any time soon. Cobot makers need to get creative with both sales and financing for SMEs.

Both traditional industrial robots and cobots are worthy of investment during such a down time. They can only go but up. Industrial robots in brisk traffic by Q4; cobots not so much by Q4, but both are the keys to automation and deserve consideration.

Then there’s Asia

A full 60 percent of all industrial robots are made in Asia and a full 60 percent are sold there, 50 percent of which go to China.

Automation is key to Asia’s collective future and robots are automation’s primary ingredient. Asia will buoy up robot sales until North America, followed by the Eurozone, come online again.

There’s time yet to invest in robots, but not much.

The breakout is a skinny seven months off.