Tumbling prices, then, should make it easier to buy an industrial robot, thereby creating solid demand for many more.

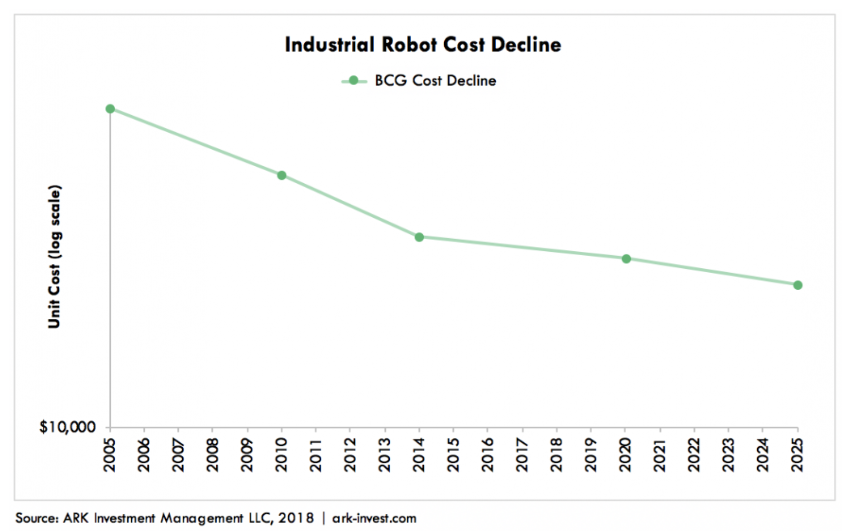

Of course, manufacturers may groan ever more loudly in the realization that their $31,000 industrial robots are selling for only $11,000 apiece. SMEs (producers of 70 percent of the world’s goods) will enjoy the price drop, and their demand for automation will accelerate sales dramatically. But SMEs, for the most part, don’t need the big-boy-size industrial robots; they want cobots.

Since in all of 2017 barely 3,000 cobots were sold in China (the same China that bought 138,000 big-boy robots), look for cobot sales to soar. Any robot manufacturer without a credible cobot in its catalog is in for a tough go of it.

Asia’s drive for productivity and competitiveness, plus the demographic time bomb of vanishing factory workers, will keep robot-driven automation alive and well throughout Asia.

When car and cellphone production slump, it’s not the end of the world for robot and robot parts sales. Diversification has taken hold. “Non-automotive industries cumulatively experienced more than 20 percent growth in orders during the first three quarters of 2018, compared to the same period in 2017.” Diversification is slated to accelerate to pharma, healthcare, agriculture, food production, etc. In short, anywhere and everywhere that needs to operate leaner and better will automate sooner than later.

The International Federation of Robotics is forecasting a population of 3.1 million industrial robots on the job globally by 2020; 2 million of them in Asia.

If Wright’s Law holds true, the increasing world population of industrial robots will be cheaper to buy, but none or very few of the 3.1 million will be “smart”.

Smart 4.0 manufacturing won’t tolerate “dumb” robots on the job, so how will all those dumb industrial robots get a few smarts? Smart grippers as add-ons? Maybe. Retrofitting industrial robots deserves strong consideration as a major new industry in the offing.

And for all of those who put stock in numbers like how many industrial robots per 10,000 workers, it may now become how many “smart” robots per 10,000 workers.

And “smart” is an industry that’s just getting going.